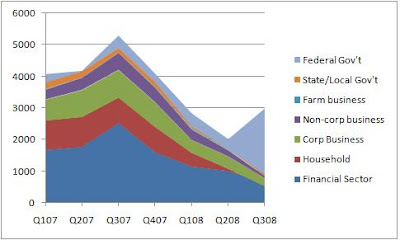

The first thing that stood out was how severe the credit contraction was. This chart is total net borrowing for years 2004-2007 and September 2008.

Here is the same chart with quarterly info from beginning of 2007 to Q3 2008:

Here is the same chart with quarterly info from beginning of 2007 to Q3 2008:

Frankly, based on these charts, I can't believe they weren't acting earlier in the year in more significant ways. It does explain why they took over Fannie & Freddie, right or wrong. Fannie and Freddie were a little bit like Ponzi schemes - they were solvent as long as they were growing. Once they started shrinking, they were wildly overexposed on their collateral base.

The Fed was pretty busy in Q3. $2 trillion and they won't say where it went. Some say that number could rise to $5 trillion as they attempt to fill the gaps as household net worth shrinks at the fastest pace in the last 20 years by a very wide margin.

With the stock market losing another 25% in the 4th quarter, and real estate on a continual decline, we could be looking at household net worth reductions from the Q3 '07 peak on the order of 15-20% in Q4, more likely the high side. From 2004-2007, personal consumption represented 14.9%-15.7% of household net worth. In the first quarter of 2008, household net worth had declined 6.1% from the peak, yet personal consumption continued to climb, albeit at decreasing rates, such that personal consumption as a percent of household net worth had increased to 18% in the third quarter of 2008. If the consumer is able to contract personal consumption to stay simply within 18% of household net worth, after considering a likely significant drop in Q4, Q4 GDP could shrink as much as 5% over the prior year same quarter.

What seems more likely is that the consumer will not be able to cut spending as fast as his net worth had declined, and consumption could exceed 20% of household net worth. In this case, Q4 GDP would grow by about 2.1%. The Fed is rooting for the very thing that we've learned to despise - overextended consumers.

Disposable income declined in the third quarter as compared to Q2, but over the prior year grew by 4.4%, within the range (although near the low end) of recent historical measures. As unemployment increases, this has to get worse. The 4th quarter data may be difficult to interpret; there could be a large portion of severance included in the disposable income figure, which could make the situation appear less ugly than it really is. On the other hand, going into the 1st quarter of 2009, all those fat CEO bonuses that the public has decried won't be in the numbers, and that will move the needle. But we won't get the Q1 figures until June, and by then we ought to know a lot more about the timing and probability of a recovery.

The only good news on the household balance sheet is that foreclosures help the balance sheets by removing mortgage debt that is greater than the value of the property listed as an asset. (If the property weren't over-mortgaged, then they could sell the house for a profit rather than submit to foreclosure). I find it a little ironic that the Fed and Congress want to see foreclosures stopped when they seem to provide a potential way out of this mess for the overleveraged consumer. Sure, permitting continuing real estate valuation declines is bad for everyone. However, the premise implies that you believe that the Fed can "permit" or "disallow" it in the first place. There is little evidence that any program targeting home price stabilization is going to work. Lower rates seem to only benefit those that are not over-leveraged, since underwriting standards are coming back to reasonable levels and no one that needs to refinance to avoid foreclosure can qualify for one. Further, there really isn't the inventory in the mortgage secondary markets to support a refinance boom if one were to occur. So, the best case scenario is that the Fed & Treasury funnel mortgage subsidies (in effect) through Fannie & Freddie, which just leaves everyone with higher tax bills in the future to pay for all these subsidies.

I read that more companies are moving to 4-day workweeks to save some employees and maintain their access to skilled labor. I don't know how this will play out in the unemployment statistics, but I'd be watching for the impact on personal disposable income in the coming reports.

The situation is simply this: If the Fed does not manage to prop up asset values to make up for a substantial portion of the household net worth that has been lost, the consumer will have no choice but to reduce personal consumption to pay down debt and increase savings. Personal consumption has represented 70% of US GDP fairly consistently since 2004, yet GDP growth has shrunk every year since then. One of the reasons that it is so consistently 70% is that any move by the consumer is matched with moves in industry, so a dollar of reduction in consumer spending has the impact of taking $1.40 out of the economy. Therefore, any serious contraction in personal consumption will set off a nasty spiral of lower GDP, which requires the consumer to reduce debt, which requires reduced personal consumption and the cycle continues. This seems to be a reasonably probable scenario at this point. By the time the Fed, Treasury and Congress' stabilization and stimulus initiatives show any impact, we may be starting from such a low point that it only has the effect of slowing the contraction of the economy, rather than reversing the contraction.

I also recall the commitment of the G-20 to avoid protectionist practices, as protectionism has been identified as the great mistake of the great depression. Since then, just about every country with an auto industry has provided support to its own manufacturers. Recently, the same is happening in the chip sector. "Buy American" will eventually be what returns us to a nation that produces enough products to support a growing economy, and if that isn't protectionist, I don't know what is.

Some really funky changes are likely to happen in the Z-1 report in the next two quarters as commercial enterprises like GMAC get reclassified as bank holding companies. I have no idea how this will manifest itself except for two things: If it results in a "bad" economic datapoint, the press will be given the explanation that the figure is not comparable due to the change, and if it results in a "good" economic datapoint, no one will pick it up and report on it and some false optimism will result.

Monday is too far away to make any predictions about the market movement this week. The typical tax selling might have been done a while back - folks will have more than enough realized losses to offset gains. Volume is supposed to pick up this week, I bet it doesn't. I think everyone is sitting on their hands until 2009. Best case, we "fall up" like we did 12/24 and 12/26. It's hard to imagine a big move in either direction this week. Enthusiasm for the inauguration will be what drives the markets higher, which will set up a harder fall when we deal with the realities of the economy, particularly as predictions of a recovery "in the second half of 2009" become "early 2010."

Joe

No comments:

Post a Comment